Repurposing an existing drug – Pentosan Polysulfate Sodium (PPS) greatly improves chances of clinical success Repurposed drugs have a 2.5 times better chance of being successfully commercialised. With over 60 years of global sales, PPS has a host of human data and an excellent safety profile.

PPS has an excellent safety profile - This well known safety profile should lead to a significantly lower cost of development, reduced clinical trial timelines and a reduced risk of clinical failure.

Short and inexpensive trials enables Paradigm to achieve clinical milestones much quicker than typical biotechnology companies Shorter/cheaper trials result in less dilution, translating into far greater shareholder returns upon a successful licensing agreement.

Targeting very large addressable markets in excess of US$14.5B+ - PPS is set to be a new, multi-acting treatment for bone marrow edema (est >US$2.5B market), a condition currently with no effective treatment and allergic rhinitis – Hay fever (>US$11B market), CHIKV/RRV (est US$1B market). COPD and Asthma are further likely indications.

The new alphavirus program further diversifies Paradigm - Five patients with RRV-arthralgia (joint pain) have already been treated with PPS under SAS demonstrating tolerance and potential clinical effects. Phase II trials to commence in short term.\

Compelling Pre-clinical and clinical data indicates PPS could be very effective treatment in humans with Hay fever, BME and viral arthritis/alphavirus – Pre-clinical data has shown PPS to be the same if not better than comparator drug – Budesonide. Furthermore, PPS was shown to be as-good-as or better-than the leading intranasal corticosteroid, AstraZeneca’s Rhinocort® / Budesonide.

Multi-faceted IP strategy IP strategy covers manufacturing, formulation and delivery patents, protecting Paradigm from competition. Exclusive rights over the only FDA-approved version of PPS (bene pharmaChem) for use in humans, ensure protection of Paradigm’s position.

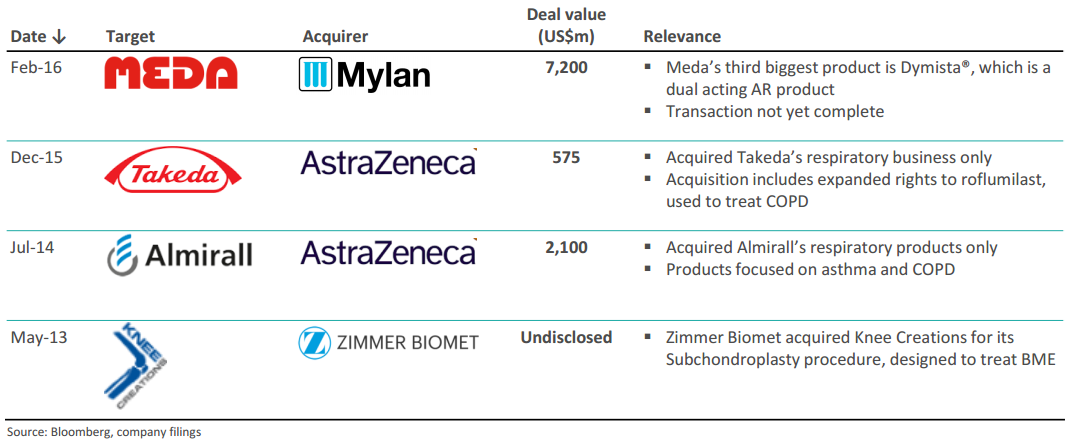

Recent Transactions highlight big pharma interest in respiratory and BME spaces - Generic drug maker Mylan NV (MYL.O) acquired Meda AB (MEDAa.ST) in a US$7.2 billion cash-and-stock deal that was a 92% premium to last close. One of Meda’s main drugs was Dymista® which is RHINOSUL®’s closest comparative product.

Highly experienced board and management team that have delivered large licensing transactions - Paradigm’s board and senior management have held positions with top ASX listed companies, CSL (CSL.ASX) and Mesoblast (MSB.ASX) and were part of the team that executed the US$1.7B Cephalon partnership.

Managing Director Paul Rennie has indicated that he will subscribe for 400,000 shares ($200,000) in this placement on the terms listed above, subject to shareholder approval at the upcoming AGM. Remaining Board and Management has indicated their intention to participate in the proposed Share Purchase Plan.